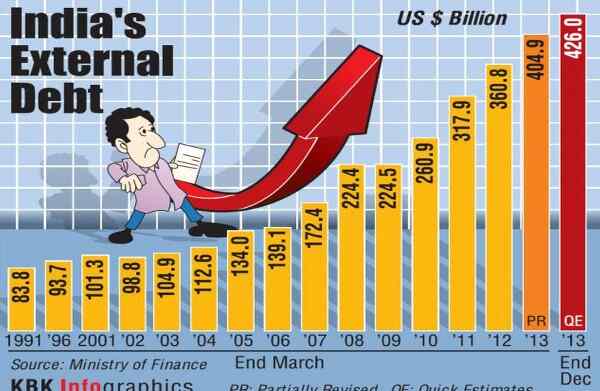

The IMF, in its latest assessment, has expressed deep concern over India’s debt trajectory, emphasizing the urgency of implementing effective fiscal measures to curb further escalation. The International Monetary Fund (IMF) has issued a cautionary note as India’s debt reaches an ALL-TIME-HIGH of ₹205 lakh crores in 2023.

IMF warns that India’s general government debt could surpass 100% of the gross domestic product(GDP) in the medium term, the Business Standard reported. These escalating levels raise significant concerns about the country’s economic stability and fiscal health.

IMF and its report

International Monetary Fund (IMF) is an internatrional fimamcial nstituion and a major financial agency og thr United Nationa. The organisation promotes economic growth, financial stability, international trade and poverty reduction. To achieve sustainable growth and prosperity for all its 190 member countries, it is regarded as the global lender of last resort.

The IMF has sounded a clear warning about the implications of India’s mounting debt. As per the Article IV consultation report by the IMF earlier, while the budget deficit has eased, public debt remains elevated and fiscal buffers need to be rebuilt. The combined debt of central and state governments stood at 81% of GDP in 2022-2023 from 88% in 2020-21.

However, the data shown is high, it is noteworthy that the same report indicates that under favourable circumstances, the IMF reckons this could even go down to 70% by 2027-28.

Response from the government

The response from the government especially the finance ministry is in total disagreement with the IMF report. India has rebuffed the International Monetary Fund’s (IMF) projection about the nation’s debt level. According to them, the situation in India is not as alarming as projected and highlighted.

The ministry highlighted the positive fiscal trends and affirmed its commitment to achieving fiscal consolidation, aiming to reduce the fiscal deficit below 4.5 per cent of GDP by FY26. The Union Finance Ministry said that the predictions by the UN’s financial body correspond to a worst-case scenario which is not a “fait accompli” or not something that can be revived.

The government also emphasised the fact that the country’s general debt is overwhelmingly rupee-dominated with minimal bilateral or multilateral borrowings from external sources. The rollover risk is low for domestic debt, and the exposure to volatility in exchange rates tends to be on the lower end.

Causes behind the debt

The surge can be attributed to a combination of factors. One of the primary causes is extensive government spending. This can be due to the increased expenditure In response to the challenges posed by the COVID-19 pandemic, infrastructure projects, welfare programmes etc. To meet immediate needs after the global pandemic such as healthcare spending, income support etc led to the situation of borrowing.

Factors such as insufficient revenue generation have also exacerbated the situation. The gap created between revenue and expenditure widened. Demographic and social factors such as the growing population increased pressure on the existing resources, and demographic shifts have impacted the budget and potentially contributed to the cause.

Impact on public investment and economy

If the debt burden becomes too high relative to the country’s economic capacity, it could lead to difficulties in repaying loans and services interest, posing a threat to overall economic stability. A substantial public debt burden may lead to higher interest rates, crowding out private investments.

Public investments, especially in infrastructure projects, could face cutbacks or delays due to budgetary constraints. Further, it leads to challenges in generating employment opportunities, especially in sectors highly dependent on government spending.

The situation poses vulnerability to economic shocks. If a significant portion of the debt is denominated in foreign currencies, the IMF may highlight potential vulnerabilities in the external sector. Exchange rate fluctuations could impact the cost of servicing foreign debt, posing additional risk to the economy. Events like the global financial crisis and geopolitical tensions like the Russis-Ukraine war have impacted the global economy.

Conclusion

The IMF‘s warning serves as a global reminder of the interconnectedness of economies and the importance of concerted efforts to address economic challenges on a broader side. India’s situation demands immediate attention and strategic interventions. Experts suggest that a comprehensive strategy is required to manage and reduce the burden effectively.

The International Monetary Fund’s caution underscores the need for proactive measures to ensure long-term economic sustainability and resilience against unforeseen challenges. The coming month will be crucial as India takes a course to manage its debt and pave the way for a stable and prosperous future.

-TANYA SHAH AND RIYA SINGH

MUST READ: UNION BUDGET 2023 ALLOCATION FOR EDUCATION IN INDIA